Replace, Integrate, Create: 3 paths Agentic Payments

which path does agentic payments actually take from here?

AI agents have settled 176 million payments through the x402 protocol, median size one to ten cents.

Bulls quote that number as proof of a boom.

Bears point out that on-chain analysts flag most of the volume as wash trading and infrastructure testing, with organic activity still tiny.

Here’s the thing: for anyone deciding where to build or invest, that debate matters less than it seems. Whether today’s volume is 20% real or 80% real, it’s a rounding error against the $33T that stablecoins moved in 2025 and either way, the same question decides everything: which path does agentic payments actually take from here?

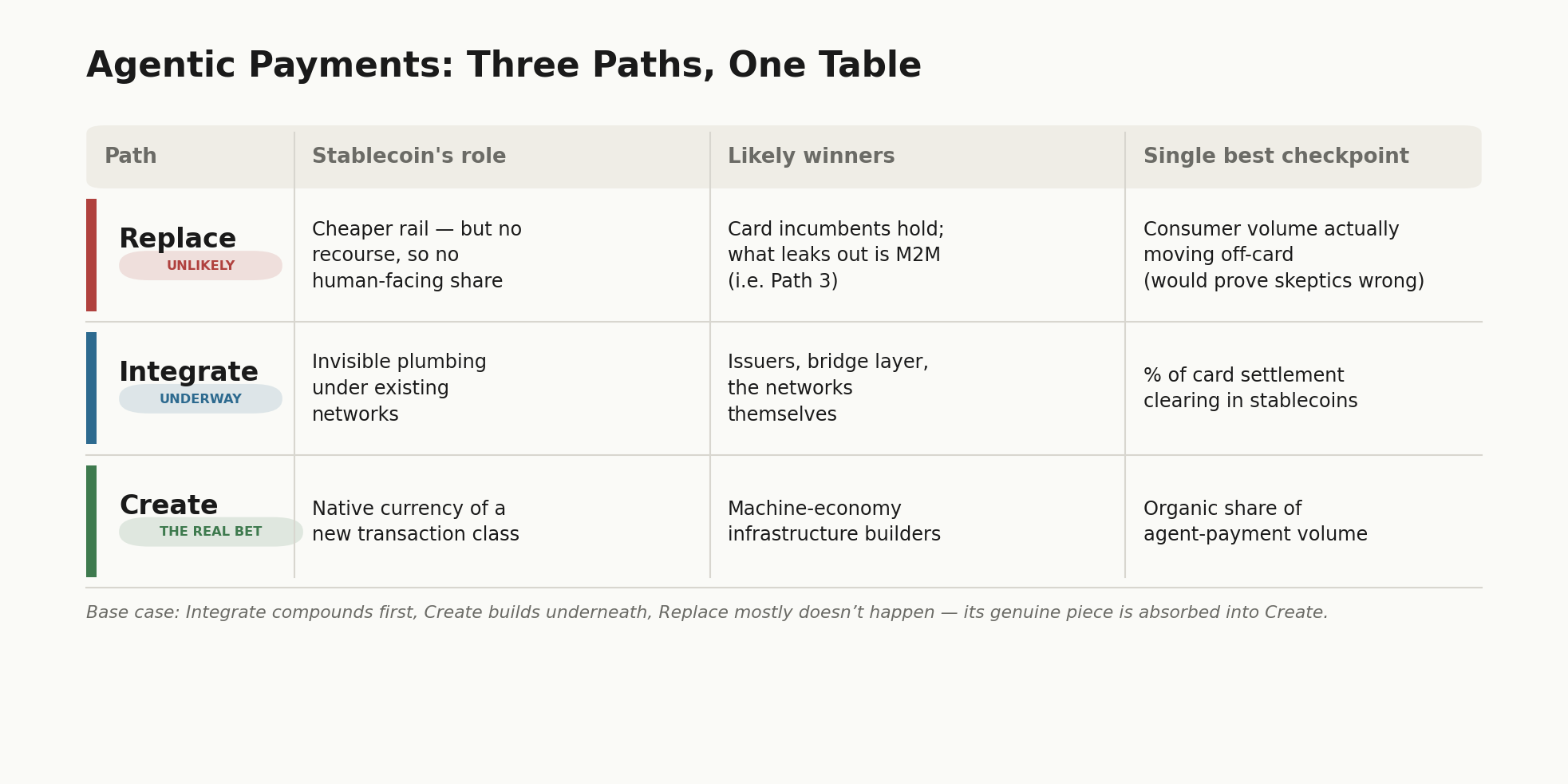

Because it isn’t one bet. It’s three distinct paths - Replace, Integrate, Create with different winners, different risks, and a different role for stablecoins in each. Most of the noise on this topic comes from people arguing about different paths without realizing it.

A few facts frame all three. The rail demonstrably works: 76% of x402 activity sits below the ~$0.30 fixed cost of a card transaction — commerce that card rails cannot price at all — and USDC settles 98.6% of it. The human-facing side of agent commerce is real but card-native: ChatGPT Instant Checkout and Google’s Universal Commerce Protocol run on traditional rails. And the whole category is gated on autonomy that’s still being built.

So: the rail works, demand is embryonic, the narrative is ahead of the data.

Now the map.

Path 1: Replace

The hypothesis: agents are cost-optimizers. They’ll notice the 2–3% merchant fee on card rails and systematically route around it.

I don’t buy it. Two reasons, one small and one fatal.

The small one: the math is less dramatic than the headline. The famous 2–3% mostly isn’t the networks’ money — interchange flows to issuing banks; the network’s own take is closer to 12 basis points. Even if agents rerouted 1% of Visa’s ~$17T, Visa itself loses roughly $200M against ~$40B in revenue. The real exposure sits in the issuer interchange pool and the rewards programs it funds — painful for banks, survivable for rails.

The fatal one: someone has to be liable. When an agent buys the wrong flight with your money, you don’t want the cheapest rail — you want someone to call. A stablecoin transfer is final: no chargeback, no issuer, no institution obligated to make you whole. And that’s not a missing feature crypto will eventually ship. Recourse requires a balance sheet that voluntarily absorbs losses — and the moment you bolt one onto a crypto rail, you’ve rebuilt the card network with extra steps. The incumbents understand this perfectly: Amex now backs both consumer and merchant when a registered agent errs; Visa shipped agent identity verification at checkout. No regulator has assigned liability for autonomous purchases, and the incumbents are converting that unsolved question into their moat.

So my read: Replace doesn’t happen anywhere a human bears the loss. What survives of it is pure machine-to-machine flow — sub-cent, nothing to dispute, no one to refund — and that isn’t a frontal assault on cards at all. That’s Path 3’s territory.

Checkpoints — that is, what would prove me wrong: a major agent platform routing meaningful consumer volume off-card; a credible liability framework that makes irreversible payments safe for humans; issuer rewards economics visibly compressing.

Path 2: Integrate

The hypothesis: stablecoins don’t fight the card networks — they become the settlement plumbing underneath them. Spend stays on cards; settlement moves on-chain.

The evidence is a progress report, not a forecast. Visa expanded its stablecoin settlement pilot to nine blockchains, explicitly positioning itself as a common settlement layer across them. Mastercard acquired BVNK and Stripe bought Bridge. The networks are jointly backing a new stablecoin platform. Stablecoin-funded card programs are already live in 18 countries — users spend stablecoins at 175M+ acceptance points while merchants settle in local fiat.

But “most certain” is not “risk-free,” and two risks deserve more airtime than they get.

Regulatory: settlement concentrating on stablecoins means concentrating on stablecoin issuers — that 98.6% USDC share is a systemic dependency on one company’s reserves and regulatory standing. And jurisdictions are diverging: if any major market decides to treat stablecoin settlement as shadow banking or an AML bypass, Integrate doesn’t die — it fragments by geography, which kills much of its point.

Technical: card settlement today is batch and forgiving. Machine commerce wants real-time. Chain finality, fee volatility, and cross-chain bridging are tolerable for T+0 batch settlement, but unproven for high-frequency clearing at card-network scale. The nine-chain abstraction play is itself a tell: the networks don’t believe any single chain is ready to carry this alone.

Checkpoints: the share of card settlement volume actually clearing in stablecoins; whether the networks’ agent protocols default to stablecoin settlement; bridge-layer M&A continuing at premium prices; a second issuer reaching scale (de-concentration from Circle).

Path 3: Create

The hypothesis: the biggest prize isn’t redirecting existing payments — it’s transactions that never existed. A research agent paying $0.005 to a niche data API it discovered thirty seconds ago. GPU time metered by the second. Agent-to-agent task outsourcing. No procurement process and no card rail could ever price these; they’re not displaced volume, they’re new TAM. And there’s a path-dependency kicker: agents won’t shop like tourists, they’ll trade like businesses — and relationships born on stablecoins stay on stablecoins, because flows born on-chain have no legacy rail to return to.

The verification problem is a cold start. Create faces a brutal chicken-and-egg: who opens the first pay-per-call endpoint, and who accepts half a cent from an anonymous agent with no relationship and no recourse? Supply won’t come without agent demand; agents can’t demand what nobody sells. (That manufactured x402 volume from earlier? Read charitably, it’s this problem made visible — when organic demand doesn’t exist yet, participants simulate both sides at once.)

And the demand gate is autonomy itself: only about a quarter of enterprises run truly autonomous agents today, maybe half by 2027. Until the human leaves the loop, the loop pays with the human’s card.

Checkpoints: autonomous (not supervised) deployment numbers; non-crypto companies opening pay-per-call endpoints; the organic share of agent-payment volume rising; a real billing-and-credit layer emerging for machine commerce.

The whole framework in one table

These paths aren’t mutually exclusive — the likeliest future is all three running in parallel at different speeds: Integrate compounding first (it’s underway), Create building slowly underneath, Replace skirmishing at the issuer-pool margins for years.

One test cuts through most stablecoin debates along the way: does this flow have a trusted intermediary everyone can accept? Where yes, stablecoins compete on cost and speed — and may win or lose on the merits. Where no — cross-ecosystem, sub-threshold, machine-speed, no human to sign up for anything — they’re frequently the only rail that exists on day one. Both situations are real. They’re just different markets.

Where to look

Directions, not picks:

The control layer. Every path — card-settled or chain-settled — needs the same thing: scoped spending authority for agents, with limits, permissions, and audit trails. The killer-product question is behavioral, not technical: how much money will a human actually delegate to an agent, and under what guardrails? Whoever answers that defines the product category. Rail-agnostic, which makes it the safest exposure to the entire theme.

The billing layer. Metering, reconciliation, statements, credit, arbitration for machine commerce. The rail works; the financial operations around it don’t exist yet. This is the most acknowledged gap in the entire stack — including by the people building the rails.

The bridge layer. Stablecoin↔fiat orchestration is crowded and getting acquired fast — but two ten-figure exits already proved the buyer demand. Legible exits, compressed timelines.

The checkpoint discipline. The cheapest position of all: don’t pick a winner yet. Every checkpoint above is public and observable. Define in advance what you’re watching for, and the market will tell you which path is compounding.

If you build, build what makes the real volume grow: the billing, the authorization, the trust plumbing that finally lets a human leave the loop.

The interesting question was never whether agents will pay with crypto. It’s which transactions exist only because they can — and right now, someone still has to build the reasons.